- The vast majority of wine is not fine wine.

- Fine wine is defined by its quantity, quality and economics, making it a financial asset as well as a luxury beverage.

- Most wine is produced for immediate consumption and lacks the structural components to improve with age, whereas fine wine is crafted to evolve over decades.

At its heart, all wine is designed for pleasure – made to be drunk and enjoyed – yet fine wine extends that experience beyond the glass, offering the potential for evolution, rarity and lasting value.

The vast majority of global wine production, estimated over 95%, is intended for the dinner table. This comprises most wines found in supermarkets, restaurants and even local wine shops. These consumer goods are made to be consistent vintage and after vintage, accessible, and best enjoyed shortly after purchase. The wines are often fresh, fruit-forward, and technically sound. They satisfy the palate but are not built for the cellar.

Meanwhile, in the territory of fine wine, the product shifts from a perishable beverage into a durable asset. This distinction is the bedrock of the wine investment market. Fine wine sits at the very top of the quality pyramid and is the result of specific environmental conditions and craftsmanship that cannot be mass-produced.

Fine wine has ageing capacity

A primary difference between standard wine and fine wine is the capacity to age.

Standard wines often have a shelf life of just two or three years. Most wine does not become better with time; it simply gets old. There is no reward for holding a basic Pinot Grigio in your cupboard, which is best enjoyed the year after harvest.

Fine wine operates on a different chemical timeline. It possesses high levels of acidity, tannins, and concentrated fruit flavours and aromas, which act as preservatives and structural supports. Over time these components interact, change and create complexity. Ironically what can make fine wine difficult to enjoy in its extreme youth is what makes it exceptional once it has aged.

With ageing, more red fine wines see their primary fruit flavours transform into complex tertiary notes like forest floor, tobacco, and truffle. This evolution is what drives the value of the bottle. Moreover, the wine becomes more desirable as it nears its peak drinking window and supply diminishes as it is consumed.

How fine wine changes with age

- Phenolic polymerization: Small tannin molecules bond together to form longer chains, which significantly reduces astringency and creates a smoother mouthfeel.

- Controlled oxidation: Small amounts of oxygen pass through the cork and slowly break down primary fruit compounds and change colour pigments.

- Esterification and hydrolysis: Continuous reactions between alcohols and acids synthesise new scent compounds, shifting the wine’s aromas from primary fruit to more complex tertiary aromas.

- Anthocyanin complexation: In red wines, red pigments bond with tannins causing the wine’s colour to shift from vibrant purple-red to garnet or tawny.

- Colloidal precipitation: As molecules grow they form insoluble sediments which settle at the bottom of the bottle.

Fine wine gets scarcer

The scarcity of aged bottles also plays a critical role in the investment reality.

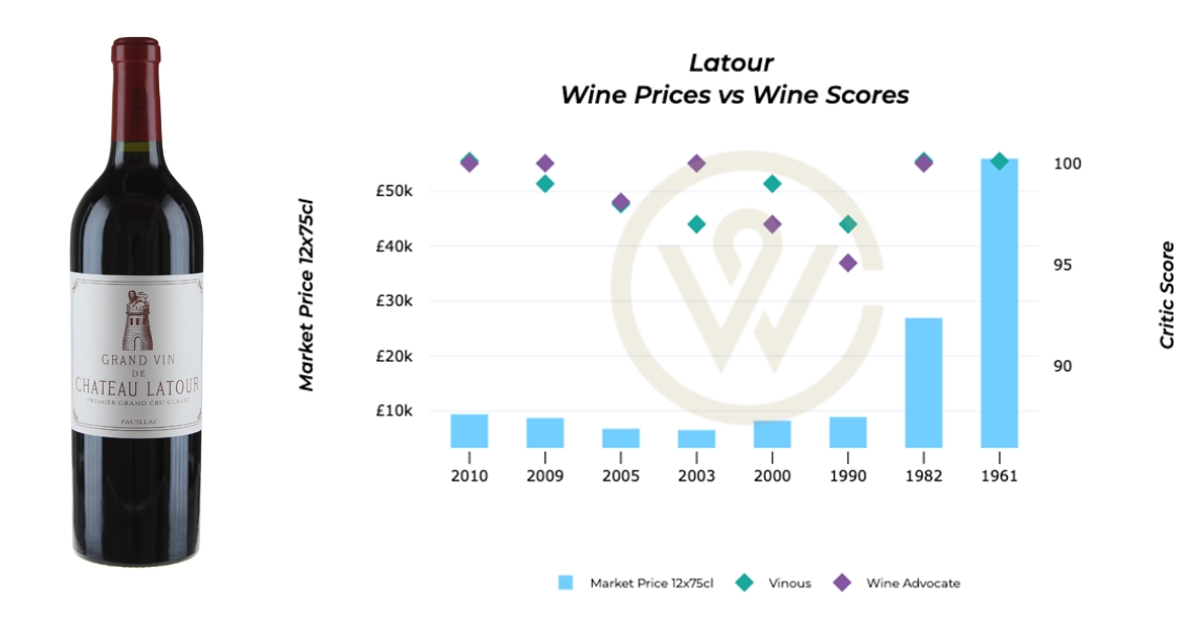

As a vintage is consumed, the number of remaining bottles in the world decreases. When you combine increasing quality with decreasing supply, you create the perfect conditions for price appreciation. This is one of the reasons why a rare 80-year-old Domaine de la Romanee Conti recently sold for nearly a million dollars at auction, while a young bottle is closer to $10,000.

Standard wine can never benefit from this change in the supply/demand dynamic because it cannot survive a journey it was never intended to make.

Fine wine has a sense of place

Fine wine is almost always tied to a specific patch of land. In regions like Burgundy, the difference between an investable Grand Cru wine and a Village wine made for short-term drinking can be a matter of a few metres. This is the concept of terroir. It encompasses the unique soil, the slope of the land, the local climate and seasonal weather, and cannot be replicated.

This regional tie creates a natural limit on supply. The land is fixed and protected by strict local laws. For instance, Domaine de la Romanee-Conti’s flagship wine Romanee-Conti can only come from one specific 4.5 acre vineyard. This restriction makes the wine a rare commodity.

In contrast, most wines designed for early consumption are made from grapes sourced across entire countries or even continents, prioritising volume over the unique characteristics of a single site.

The blending exception

While terroir is the rule, there are notable exceptions where fine wine is defined by the skill of the blender.

- Champagne is the most obvious of these. While many top-tier reds rely on tiny vineyard plots, iconic houses like Dom Perignon produce significant quantities with grapes from plots across the region. This allows cellar masters to create a consistent, complex profile that ages for decades.

- Penfolds Grange is another famous example. Unlike the single-vineyard focus of Bordeaux and Burgundy, Grange is a multi-regional blend. The winemakers source the best Shiraz grapes from various locations across South Australia to create a consistent house style. Despite lacking a single-vineyard origin, it is a highly collectible wine.

Fine wine is not solely about where the grapes are grown. While geographic specificity is an indicator, the ultimate test is the quality of the finished product and its ability to age gracefully.

Fine wine has producer reputation

Reputation is the currency of fine wine. A standard wine might be delicious, but without a historical track record, it cannot be considered an investment. Meanwhile, fine wine estates have often spent centuries building their brand: the 1855 Classification in Bordeaux is still a guide for investors today. It provides a hierarchy that the market trusts and gives buyers the confidence that the wine will perform as expected.

Fine wine attracts critical attention

Critic scores are a modern extension of this and provide crucial information for investors and collectors. A high score from a respected publication can cause an immediate spike in market value; a series of high scores over a number of years might elevate a wine to be considered a fine wine.

Even so, most wines rarely receive this level of scrutiny. If they are reviewed at all, the assessment might focus on whether they are pleasant to drink right now, rather than on their structural integrity and ageing potential.

Fine wine is more complex

The flavour profile of fine wine is noticeably more complex than that of everyday bottles. Standard wine tends to be more linear: you might taste strawberry or lemon or apples, and that flavour remains consistent from the first sip to the finish.

By contrast, fine wine is often described as multidimensional. It offers layers of smell and flavour that reveal themselves slowly as the wine sits in the glass.

Fine wine also possesses length. This is the duration that the flavours linger after you have swallowed. In a standard wine, the flavour might vanish in seconds, while in the best fine wines it can last for minutes.

This is another hallmark of high-quality winemaking. It indicates a level of concentration and balance that is impossible to achieve in mass-market production. The sensory experience is simply deeper and more rewarding.

Price differential

It is a common myth that all fine wine is expensive. While “blue-chip” labels like Petrus or Le Pin can cost thousands of pounds, the entry point for fine wine is often more accessible than people think. Fine wines from regions like Bordeaux or Rioja often sell for well under £50. These wines offer the same ageing potential and structural complexity as their more famous peers, and while they may not be investable, they could still be categorised as “fine wine”.

Beyond cost, there is the question of value. For instance, a £10 bottle of supermarket wine has zero re-sale value the moment you leave the shop. A £60 bottle of high-quality Barolo not only has the potential to double or triple in value over a decade but will leave a lasting impression when consumed.

Put simply, fine wine is an asset, whereas standard wine is an expense. The higher upfront cost is an investment in a product that can preserve and grow your capital, as well as deliver a different quality of drinking pleasure.

Quality vs quantity

Fine wine relies on the natural concentration of the grapes. This concentration is achieved by keeping vineyard yields low, which increases the cost of production.

Low yields mean fewer bottles of higher quality and is the fundamental trade-off of the fine wine world. A mass-market producer wants to harvest as many grapes as possible to fill as many bottles as they can, while a fine wine producer prunes the vines aggressively to ensure the remaining grapes are packed with flavour and structure.

This focus on quality over quantity is the most significant contrast between fine wine and standard wine.

From consumer to collector

Moving from simply drinking wine to collecting and investing in fine wine requires a clear shift in mindset. The focus moves away from what to open tonight, towards what will reach its peak in a decade or more. While the pleasure of fine wine still lies in the glass, it also comes from something deeper – the ability to follow a wine’s evolution over time. Fine wine is a living, changing asset, and that sense of development and anticipation is something few other wines, or indeed other alcoholic products, can truly offer.

FAQ

Can a cheap bottle of wine ever become “fine wine” if I leave it in a cellar?

No. Ageing cannot create quality where it does not already exist. Fine wine must be “built” for the cellar from the moment the grapes are grown.

Is all expensive wine considered fine wine for investment?

Not necessarily. Some wines are expensive due to branding, luxury packaging, or celebrity associations but lack a secondary market. To be investment-grade, a wine needs a history of price appreciation and a global network of buyers ready to trade it.

Why does region matter so much in fine wine?

Specific regions have unique microclimates and soil that produce grapes with exceptional character. These areas are often legally protected, meaning supply is capped. This combination of unique quality and restricted supply is what creates long-term value for investors.

How can I tell if a wine has a different flavour profile without opening it?

You can rely on critical reviews and tasting notes from professional tasters. They will describe the complexity, the tannins, and the “length” of the wine. Look for terms like “structured,” “tight,” or “evolving,” which indicate a wine that is built to improve over time.

Can a blend be a fine wine?

Yes. Many of the world’s greatest wines are blends. Most Bordeaux wines are a mix of Cabernet Sauvignon and Merlot. Champagne is often a blend of different areas within the region and even from different years. Penfolds Grange is a multi-region blend. The key is the quality of the components and the skill involved in the assembly.

WineCap’s independent market analysis showcases the value of portfolio diversification and the stability offered by investing in wine. Speak to one of our wine investment experts and start building your portfolio. Schedule your free consultation today.