- In the vast world of sparkling wine, Champagne remains the global benchmark for both quality and prestige.

- The production method creates a divide: Champagne, Cava, and most English sparkling wine use the bottle-fermented “traditional method,” while Prosecco relies on the faster “tank method.”

- From a financial perspective, Champagne is the only truly investable sparkling wine on the secondary market.

Sparkling wine, fit for any celebration, is more than just a drink for a toast. It is a vast category defined by geography, history, and chemistry. While most people recognise the pop of a cork, the liquid inside that bottle can vary wildly depending on where the grapes have been grown and how it was made.

To understand the difference between Champagne, Prosecco, Cava, and English sparkling wine we have to look at what happens inside the cellar. While they all have bubbles, the way those bubbles are created changes the flavour, the texture, the price tag and the investment reality.

The traditional method: Champagne, Cava and English fizz

Champagne, Cava, and English sparkling wine are all made using the “traditional method.” This is the most expensive and time-consuming way to make wine.

- First, the winemaker creates a still dry wine.

- Then, they put it into a bottle with a little bit of sugar and yeast and seal it with a crown cap like you’d find on a bottle of beer.

- A second fermentation happens inside that specific bottle. Because the carbon dioxide cannot escape, it dissolves into the wine, creating the sparkle.

The final stage has the wine sitting on the lees: the dead yeast cells. Over months or years, these cells break down and give the wine flavours of toasted bread, brioche, and nuts. This is what experts call “autolytic” character. It is the reason why a glass of Champagne often smells like a bakery, while a Prosecco smells like a fruit basket.

Champagne: The undisputed king

Champagne is a specific region in northern France. If a sparkling wine is not from there, it is not Champagne. The region is famous for its white, chalky soil. This soil acts like a sponge, holding water but also reflecting sunlight back up to the vines.

The major grapes here are:

- Chardonnay

- Pinot Noir

- Pinot Meunier

Four other varieties are also permitted but rarely used:

- Pinot Blanc

- Pinot Gris

- Arbane

- Pinot Meslier

This combination creates a wine with incredible structure and high acidity. This acidity is the backbone that allows the wine to age for decades.

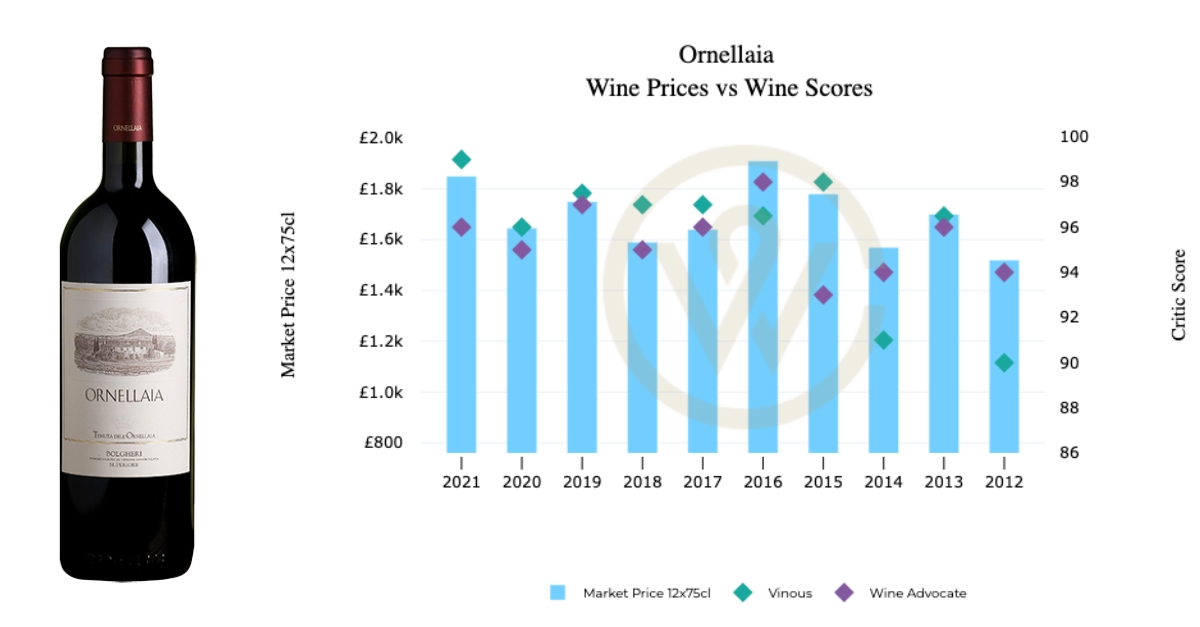

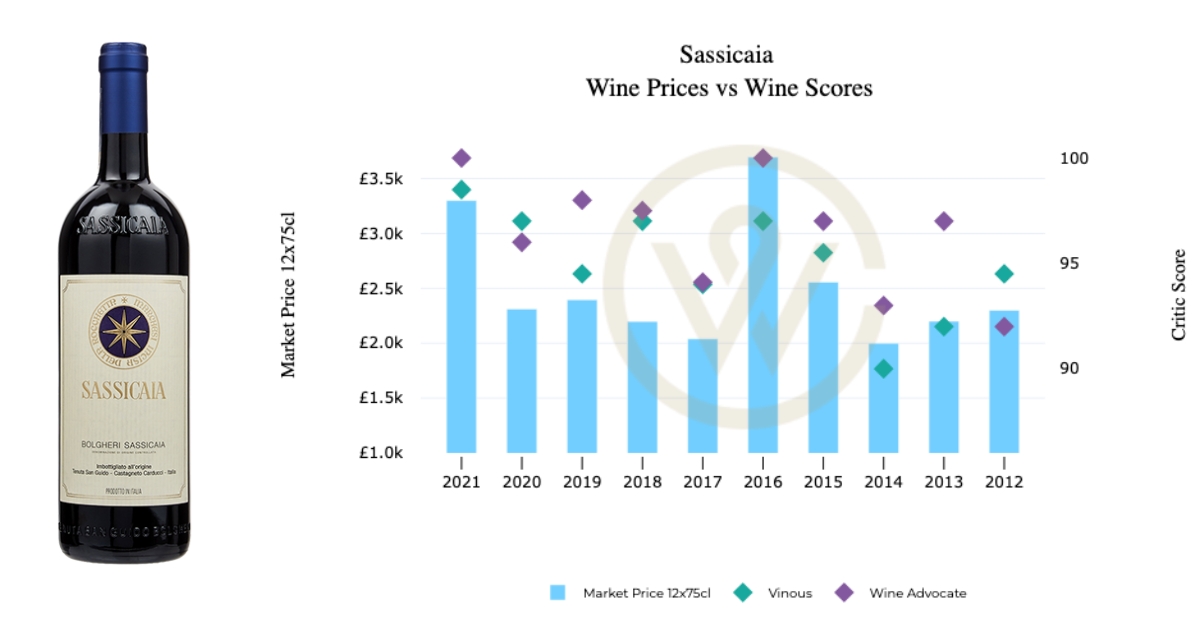

Indeed, its ageability, decades long reputation and high quality make Champagne one of the most prominent investment players on the secondary market for fine wine. Still, there is a catch.

Most non-vintage (NV) bottles, which are the standard blends houses produce every year, do not necessarily increase in value. With very few exceptions, only vintage Champagne is investable. These are wines made from grapes harvested in a single year. They are produced in smaller quantities and are built to last.

Vintage Champagnes are the primary targets for collectors and investors looking for a return.

Looking for more? Read our Champagne Regional Report.

English sparkling wine: The rising star

The story of English sparkling wine is one of geology and changing climates. The same chalk seam that runs through Champagne actually dips under the English Channel and pops up again in the South of England.

Counties like Kent, Sussex, and Hampshire have soil that is nearly identical to the best plots in France. As the climate has warmed, these regions have become perfect for growing the same three grapes used in Champagne.

- Chardonnay

- Pinot Noir

- Pinot Meurnier

The style of English sparkling wine is often very lean and crisp. It has a piercing acidity that makes it incredibly refreshing. While the quality is now world class, the market is still catching up.

Search data on Wine-Searcher shows that the most popular English sparkling wines are currently sitting just inside the top 5000 most searched for wines. Interest is growing, but it is still a long way from the global dominance of the famous French houses.

Cava: Spain’s traditional bubble

Cava is Spain’s answer to Champagne. Most of it comes from the Penedès region in Catalonia. While it uses the same traditional method as Champagne, the flavours are different because the grapes are different.

The traditional Cava blend uses:

- Macabeo

- Xarel-lo

- Parellada

These indigenous Spanish grapes often produce wines that are a bit more earthy or floral. They generally have lower acidity than Champagne or English sparkling wine, which makes them feel softer in the mouth.

Despite its long history, Cava struggles on the secondary market. It is often viewed as a value-for-money option rather than a luxury collectible. This is reflected in its search rankings: even the most famous Cavas usually sit outside the top 3000 most searched for wines globally. For an investor, Cava currently lacks the secondary market activity needed to be a viable asset.

The Charmat method: Prosecco

Prosecco is a completely different beast. It comes from the Veneto and Friuli regions of Italy and is made using the “tank method” (also known as the Charmat method).

Instead of the second fermentation happening in a bottle, it happens in a large stainless steel tank. This is much faster and cheaper. The goal here is not to create bread-like flavours from yeast, but to keep the wine tasting like fresh fruit.

Glera must make up 85% of the blend with the rest consisting of:

- Verdiso

- Bianchetta Trevigiana

- Perera

- Glera Lunga

- Chardonnay

- Pinot Bianco

- Pinot Grigio

- Pinot Noir

The Glera grape used in Prosecco is naturally aromatic. It smells of white peach, pear, and honeydew melon. Because it does not spend long on the yeast, the bubbles are often bigger and frothier.

Prosecco is designed to be drunk fresh. It does not improve with age. Because of this, it has almost no presence in the investment world. Like Cava, the most popular Proseccos are found outside the top 3000 most searched for wines. It is a wine for the moment, not for the cellar.

Investing in sparkling wine: a guide

The difference in investment potential between these regions is striking. While you can find a delicious bottle of sparkling wine from any of these four places, the financial world only really cares about one.

Secondary market activity is the engine that drives wine investment. This involves collectors buying and selling bottles through auction houses or private exchanges. This activity requires three main things:

- Brand power: A name that people all over the world recognise and want.

- Scarcity: A limited supply that cannot meet the high demand.

- Longevity: A wine that will actually taste better (and be worth more) in time.

Champagne, specifically Vintage Champagne and “Prestige Cuvées” like Dom Pérignon or Krug, checks all three boxes. English sparkling wine is building the brand power, but it lacks the historical track record and data about its aging potential that investors crave. Cava and Prosecco, meanwhile, are produced in such high volumes that scarcity is rarely an issue, which prevents prices from climbing on the secondary market.

Other sparkling wine regions

The world of bubbles does not end with these four. Other regions are also making their mark, though they face similar hurdles regarding investment.

- Franciacorta: Italy’s premium sparkling wine made in the traditional method. It uses Chardonnay and Pinot Nero, often resulting in a richer, riper style than Champagne.

- Crémant: These are French sparkling wines made outside of Champagne. Crémant de Bourgogne (Burgundy) and Crémant d’Alsace are excellent value alternatives that use the traditional method.

- Tasmania: Australia’s cool-climate island is producing some of the most exciting New World bubbles, characterised by high acidity and elegance.

- California: Areas like the Anderson Valley produce powerful sparkling wines that often show more ripe fruit and oak influence than their European cousins.

While these wines are fantastic for enthusiasts, they currently exist outside the scope of “investment grade” wine. They are brilliant additions to a dinner party, but they are not yet staples of a financial portfolio.

Sparkling wine style: texture and taste

When you are choosing a bottle, the “mousse” or the feel of the bubbles is a great way to tell them apart.

Traditional method wines (Champagne, English, Cava) usually have very fine, tiny bubbles that tingle on the tongue. This is because the carbon dioxide has had a long time to integrate with the liquid during its years in the bottle.

Tank method wines (Prosecco) have larger, more lively bubbles. They feel more “fizzy” and can sometimes be a bit more aggressive. This is why Prosecco is so popular in cocktails like the Aperol Spritz: the bubbles are strong enough to stand up to other ingredients.

Whether you are looking for a bottle to open tonight or one to keep for a decade, the differences between these four regions are significant.

Champagne remains the gold standard and is the only choice for those looking at sparkling wine as an asset.

English sparkling wine is the exciting newcomer, offering a taste of what Champagne used to be before the impact of climate change: high-acid, lean, and intensely fresh. Cava provides a wonderful, earthy alternative for those who love the traditional method but want a different flavour profile. Finally, Prosecco remains the ultimate choice for accessible, fruity fun.

By understanding the production methods and the market data, you can navigate the wine aisle with much more confidence. The world of sparkling wine is diverse, and while only a small slice of it is “investable,” every region offers something unique for the palate.

People Also Ask

What is the main difference between Champagne, Cava, and Prosecco?

The primary difference lies in the production method and region. Champagne (France) and Cava (Spain) use the “traditional method,” where the second fermentation happens in the bottle, creating complex brioche flavors. Prosecco (Italy) uses the “tank method,” which is faster and preserves the fresh, fruity flavors of the Glera grape.

Is English sparkling wine as good as Champagne?

Yes, many critics now consider English sparkling wine to be of world-class quality. Because the South of England shares the same chalky soil seam and a similar (though cooler) climate to Champagne, it produces wines with high acidity and lean, crisp profiles that rival top French houses.

Why is Champagne more expensive than Cava and Prosecco?

Champagne is generally more expensive due to its labor-intensive production, long aging requirements (on the “lees”), and the high cost of land in the Champagne region. Additionally, its global reputation for luxury and high demand on the secondary market keeps prices at a premium compared to high-volume regions.

Which sparkling wines are best for investment?

Currently, Vintage Champagne and Prestige Cuvées (like Dom Pérignon or Krug) are the only sparkling wines with a significant track record for investment. They offer the necessary brand power, scarcity, and longevity to increase in value on the secondary market, whereas Prosecco and Cava are designed for immediate consumption.

Can you age Cava or Prosecco like Champagne?

Generally, no. Prosecco is designed to be drunk fresh to enjoy its floral aromas; it does not improve with age. While some premium Cavas can age, most do not have the same “autolytic” structure or acidity as Vintage Champagne, which is specifically built to evolve over decades.

What does “Traditional Method” mean on a wine label?

The “traditional method” (or Méthode Traditionnelle) indicates that the wine underwent its second fermentation inside the bottle. This process creates finer bubbles and distinct flavors of toast, brioche, and nuts, which are characteristic of Champagne, Cava, and English sparkling wine.

WineCap’s independent market analysis showcases the value of portfolio diversification and the stability offered by investing in wine. Speak to one of our wine investment experts and start building your portfolio. Schedule your free consultation today.