In our first quarterly summary for the year, we look at how global geopolitical instability has affected demand for safe-haven assets and how fine wine is poised to benefit. We also examine the pricing strategy of recent releases through La Place de Bordeaux, and what this tells us about the state of the market and how it sets the tone for the upcoming En Primeur campaign. Beyond the news headlines, we deep dive into this quarter’s top performers – wines that have shown resilience and, in some cases, double-digit returns.

Key findings:

- Geopolitical instability in the Middle East has driven a “flight to safety” among investors. As a tangible hedge against inflation and market volatility, fine wine is keenly poised.

- New releases from Yquem, Latour, and Bollinger have combined high quality with keen pricing strategies that prioritise market liquidity.

- Bordeaux accounted for 80% of the quarter’s top performers, led by Sauternes and Barsac.

- A consistently increasing bid:offer ratio throughout Q1 suggests the secondary market has established a solid floor and is seeing defensive growth entering Q2.

- Landmark trade deals in India and Europe are redirecting global liquidity, creating a structural foundation for long-term demand growth in the East.

- A new record-breaking auction result set by DRC 1945 at $812,500 highlighted the unprecedented value the market continues to place on rare, historic assets.

Executive summary

The first quarter of 2026 was a tale of two halves, beginning with a surge of renewed market optimism that quickly collided with a transformative geopolitical crisis. The year opened with the FTSE 100 hitting historic milestones and a “Goldilocks” cooling of inflation, but the upward trajectory of mainstream markets was abruptly severed by the outbreak of the war in Iran and the subsequent closure of the Strait of Hormuz. The conflict triggered an immediate and aggressive “flight to safety,” sending gold and the U.S. Dollar to premium levels, simultaneously forcing a dramatic repricing of global energy and supply chain risks.

As markets continue to grapple with a destabilised Middle East and investors look to navigate heightened volatility, assets that offer both tangibility and independence from traditional market shocks like fine wine can be uniquely positioned to benefit.

According to our annual wealth management survey (full results to be released next week), 50% of US and 35% of UK respondents believe that global conflict actually helps fine wine perform during periods of market volatility in the sense that it highlights fine wine’s role as a psychological and financial refuge. Fine wine’s physical nature provides a sense of security that digital or equity-based assets cannot replicate in a climate of uncertainty.

While fine wine operates on its own internal dynamics, the signs of a market recovery from within have been highly encouraging. The bid:offer ratio has continued to rise throughout the quarter, signalling increased demand and growing liquidity – both of which have underpinned price stability. As our report explores, while broader market indices remain steady, select high-performing labels have already registered double-digit returns this quarter.

Perhaps the most encouraging sign of optimism has been the sensible pricing of new releases. Vintages that offer clear relative value compared to back-catalogue stock are reinvigorating buyer appetite and restoring long-term trust. This disciplined approach to pricing sets a constructive tone for the upcoming Bordeaux En Primeur campaign – the defining event of Q2 – which we anticipate will be a critical barometer for the market’s direction in the months ahead.

What new wine releases tell us about the state of the market?

While the global economy faces external shocks, the fine wine market is providing its own internal “green shoots”. The narrative of the last six months has been one of adjustment and acceptance. We are seeing a concerted effort from major estates to meet the market where it is, rather than where they wish it to be.

This trend arguably began last summer with Taittinger Comtes de Champagne Rosé 2012. Offered at what many consider the low point of the recent market cycle, it was the first major release priced with enough sensitivity to reinvigorate trade. That successful launch set a precedent that we are now seeing echoed across the board in the 2026 Spring releases from giants like Bollinger, Yquem, and Latour.

The “Yquem Factor”: Quality meets stability

The recent release of Château d’Yquem serves as a primary example of how tangibility and quality are driving the current “flight to safety.” With a rare unanimity of 100-point scores from Wine Advocate, James Suckling, and Vinum, this “epochal” vintage is being compared to the legendary 2001. However, by coming to market at roughly 50% of the price of its 2001 peer, Yquem is offering a clear value proposition in a volatile world. This sensible entry point, combined with the fact that our Wine Track Yquem index has remained remarkably stable since early 2025, highlights the region’s role as a resilient financial refuge.

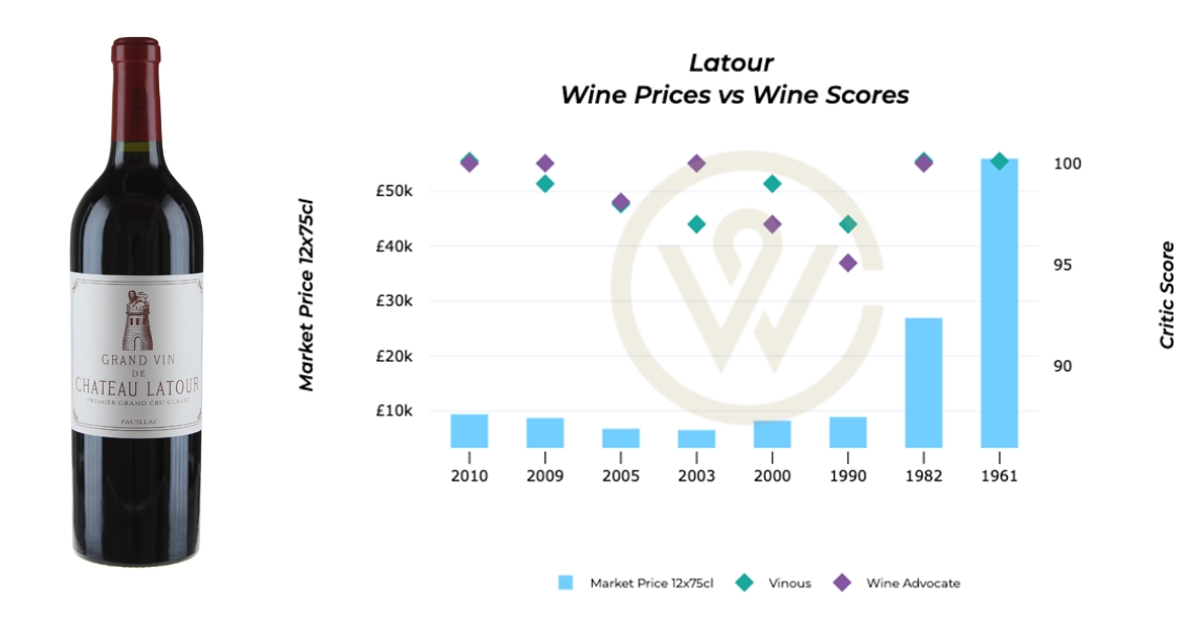

Latour 2019: The benchmark for “keen” pricing

The momentum has reached a crescendo with the release of Château Latour 2019. While critics like William Kelley describe it as a “profound wine in the making,” its true significance lies in its pricing strategy. Released at a more accessible level than any comparable back vintage, it sits 15% lower than the 2016, even as prices for the 2009 and 2010 vintages have begun to climb. By pricing the 2019 to offer immediate relative value, Latour is successfully reinvigorating trade and setting a disciplined, optimistic tone for the upcoming campaign in the region.

Bollinger La Grande Année 2018: Value in Champagne

Outside of Bordeaux, Champagne house Bollinger released its 2018 La Grande Année Brut and Rosé this March. As the first of a trio of exceptional warm vintages – drawing comparisons to the legendary 1988–1990 run – the wine arrives with significant critical weight. Boasting a 96-point score from Antonio Galloni (Vinous), the 2018 notably outperforms the prestigious 2002 and 2012 editions. Crucially, Bollinger has matched this high quality with an aggressive pricing strategy, entering the market at an approximately 15% lower cost than the most recent 2015 release. The competitive price point of the house echoes the strategy seen with Latour and Yquem, proving that producers across the board understand the importance of liquidity and building buyer trust.

Acceptance of the “new reality”

These releases signal a significant shift in the primary market. By pricing new vintages to offer relative value against existing back-stock, estates are rebuilding trust and liquidity. This discipline is being mirrored in the secondary market, where we are seeing:

- Improved trade volumes: A rising bid:offer ratio across the major exchanges.

- Sustained stability: A “floor” has been established, allowing for the double-digit returns seen in our top-performing wines this quarter.

This environment of sensible pricing and high critic consensus sets a highly optimistic tone for the upcoming Bordeaux En Primeur campaign. It suggests that the market has not just stabilised, but is actively preparing for its next growth phase.

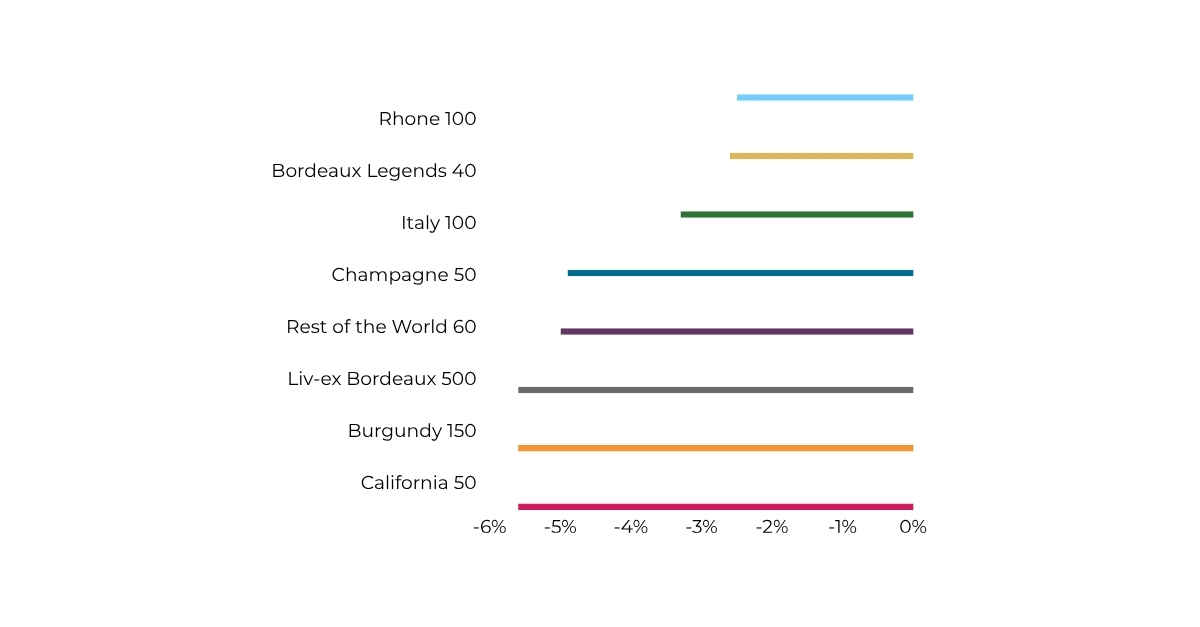

The best-performing wines of Q1 2026

While the broader market has focused on stability, a selection of labels has delivered exceptional year-to-date (YTD) growth. The first quarter was unequivocally dominated by Bordeaux, which accounted for eight of the top ten performers, showcasing the region’s enduring appeal as a primary destination for “flight to safety” capital.

The resurgence of Sauternes and Barsac

The most striking trend of Q1 has been the performance of Bordeaux’s sweet wines. Chateau Rieussec 2021 led the market with a remarkable 55.6% YTD increase, further supported by its 2013 vintage, which grew by 22.1%. This positive momentum can be tied to buyers finding value in back vintages in light of more expensive recent Rieussec releases. This trend extended to Barsac, where Chateau Coutet 2016 and Chateau Climens 2012 both posted gains near 20%. This suggests a significant re-rating of the sector as investors seek out high-quality wines that may have been previously undervalued.

Blue-chip resilience

Beyond the sweet wine categories, Right Bank powerhouses and elite Left Bank estates showed defensive strength:

- Chateau Lafleur 2016 saw a significant jump of 33.6%, reinforcing its status as a collector favourite with high scarcity value.

- Pavillon Rouge du Chateau Margaux 2013 and Chateau Haut-Bailly 2021 both delivered a robust 25% return, proving that quality second wines and top-tier Cru Classé estates remain resilient despite the wider geopolitical “re-pricing.”

Diversification beyond Bordeaux

Outside of France, top-tier international labels also found favour. Italy’s Giacomo Conterno, Barolo Monfortino Riserva 2005 rose by 21.0%, while California’s Dominus 2017 represented Napa Valley with a strong 20.1% gain.

New wine auction record

Perhaps the most significant wine event in Q1 came from the auction room, which saw a new record broken for the most expensive wine ever sold. In a definitive display of the market’s appetite for rare, tangible history, Acker Merrall & Condit auctioned a single bottle of 1945 Domaine de la Romanée-Conti (DRC) Romanée-Conti for a record-breaking $812,500 (including buyer’s premium).

This sale shattered the previous world record for a standard 75cl bottle, set in 2018. As one of only 600 bottles ever produced from this “unicorn” vintage – harvested at the close of WWII and just before the vineyard’s vines were pulled for replanting – the 1945 DRC represents the pinnacle of provenance and scarcity. The new record is a powerful reminder that even amidst geopolitical uncertainty, the world’s most historic and tangible assets continue to command unprecedented value.

Q1 wine tariffs update

A significant theme this past quarter was the shifting landscape of global wine tariffs, ranging from US policy changes and the landmark India trade deal to the evolving terms for Australian wine imports into Europe.

The US “tariff reset”

The US market began the quarter in a state of regulatory flux. In February, the Supreme Court struck down previous “emergency” tariffs as unconstitutional, only for the executive branch to immediately pivot to Section 122 of the Trade Act. This imposed a new 10% baseline tariff (with threats to rise to 15%) on almost all imported wine.

- The market impact: While this has created a “wait-and-see” approach among some US collectors, the secondary market has proven remarkably resilient. Unlike previous cycles, the market is no longer solely dependent on a hyper-active US base; instead, it is being bolstered by robust demand from Europe and Asia. Furthermore, US buying activity has shown improvement compared to the same period last year, suggesting that seasoned collectors are looking past the “noise” of temporary duties.

- The opportunity: These new tariffs are temporary by design, set to expire in late July 2026 unless extended by Congress. This 150-day window has paradoxically increased the appeal of existing “pre-tariff” stock already held in US warehouses, while the broader global market continues to find its floor through diversified international trade.

India: The next great frontier

Perhaps the most significant long-term development for the fine wine market is the newly signed EU-India and UK-India trade deals. For nearly two decades, India’s 150% federal import tariff has stood as the single greatest barrier to entry for the world’s most prestigious estates.

- The update: Under the new agreements, tariffs on premium EU and UK wines are being slashed from 150% down to 100% immediately, with a glide path to 25% over the next decade for bottles meeting specific price thresholds.

- The impact: While this policy change is unlikely to transform the market overnight, it represents a massive structural milestone. With India’s middle class projected to comprise 60% of the population by 2047, this tariff reduction provides the necessary foundation for India to eventually rival China as a primary pillar of global fine wine demand. By lowering the cost of entry, these deals open a vital new channel for liquidity and diversification at a time when traditional Western markets are facing increased volatility.

EU removes tariffs on Australian wine imports

Following years of friction, Australia and the EU finalised a Free Trade Agreement (FTA) in late March. This deal effectively removes almost all EU import tariffs on Australian wine – a move expected to save Australian exporters roughly $37 million annually.

- The trade-Off: In exchange for zero-tariff access, Australia has agreed to protect 1,600 EU Geographical Indications (GIs). Most notably, Australian producers will phase out the use of “Prosecco” on export labels over the next ten years.

- The benefit: This agreement levels the playing field for Australian “fine wine” exports into Europe, allowing high-end producers from regions like Margaret River and the Barossa to compete more aggressively with European counterparts on price.

Why this matters

As global trade becomes more fragmented, these shifts are redirecting the flow of fine wine. While US demand is temporarily throttled by domestic policy uncertainty, the “opening up” of India and the streamlined EU-Australia trade route suggest that liquidity is shifting toward the East and the Commonwealth.

Fine wine outlook for Q2 2026

The global macro environment remains defined by heightened uncertainty. With the conflict in the Middle East continuing to disrupt energy corridors, global inflation has seen a resurgence. In this high-inflation environment, the case for fine wine as a proven inflation hedge and a “tangible” store of wealth has rarely been more compelling. Unlike traditional equities, which remain sensitive to fluctuating interest rates and energy-driven volatility, fine wine’s historical low correlation to mainstream markets is expected to remain its greatest strength throughout the spring.

The Bordeaux 2025 En Primeur campaign

The defining event for the wine trade will be the Bordeaux 2025 En Primeur campaign (April–June). Following the “keen” pricing strategies established by Latour and Yquem in Q1, the industry mood is one of cautious optimism. There is a clear expectation that for the 2025 vintage to succeed, estates must continue this trend of market-aligned pricing.

- The opportunity: If châteaux offer the 2025 vintage at a relative discount to existing physical stock, we can expect a release of sideline capital into the market.

- The sentiment: Early reports suggest the 2025 vintage is one of exceptional quality, potentially providing the “high-score, high-value” combination required to sustain the market’s current recovery phase.

Industry events and global liquidity

Beyond Bordeaux, the upcoming London Wine Fair and various Asian trade summits in May will serve as critical barometers for global liquidity. We expect these events to highlight the burgeoning demand from the rest of the world, especially in light of recent tariff changes.

Solid market floor

Overall, our outlook for Q2 is one of defensive growth. While the world remains volatile, the “green shoots” identified in Q1 – sensible pricing, rising bid:offer ratios, and record-breaking auction results – suggest that fine wine has established a solid floor. Its relative isolation from traditional markets can also play in its favour, providing investors with a psychological and financial refuge that continues to command value even as mainstream markets fluctuate.

Q&A

Q: How has the war in Iran impacted the fine wine market compared to gold?

A: While gold remains the traditional “first responder” to geopolitical shocks – surpassing $5,400/oz this quarter – fine wine is also a “safe haven” asset. Its value is driven by different mechanics; while gold reacts to currency fear, fine wine reacts to the search for tangible, depleting assets. This quarter, we saw fine wine indices rise, proving the asset’s role as an effective portfolio “smoother” during times of crisis.

Q: With inflation rising again due to energy costs, is now a good time to buy?

A: Historically, yes. Fine wine has a proven track record of outpacing inflation, particularly when cost-of-living increases are driven by supply shocks. Because it is a physical asset with a finite supply that decreases as it is consumed, it naturally holds its value better than cash. With prices for many blue-chip wines currently near a five-year floor, Q1 has presented a rare “double opportunity”: low entry prices combined with high inflation protection.

Q: What should I look for in the upcoming Bordeaux En Primeur?

A: The “golden rule” for En Primeur is relative value. We are looking for châteaux that follow the lead of Latour and Yquem by offering “keen” pricing. The 2025 vintage is reported to be of exceptional quality but with lower yields due to the August heatwaves; this scarcity, combined with sensible release prices, could make it a significant investment opportunity.

WineCap’s independent market analysis showcases the value of portfolio diversification and the stability offered by investing in wine. Speak to one of our wine investment experts and start building your portfolio. Schedule your free consultation today.