- Bordeaux anchors portfolios with liquidity and stability, while Burgundy and niche producers often deliver the highest upside.

- Scarcity drives returns: from cult Burgundy to grower Champagne, the biggest gains come where supply is tight and demand is global.

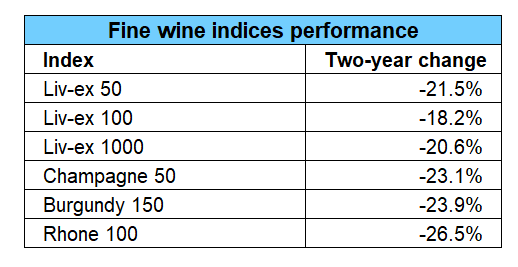

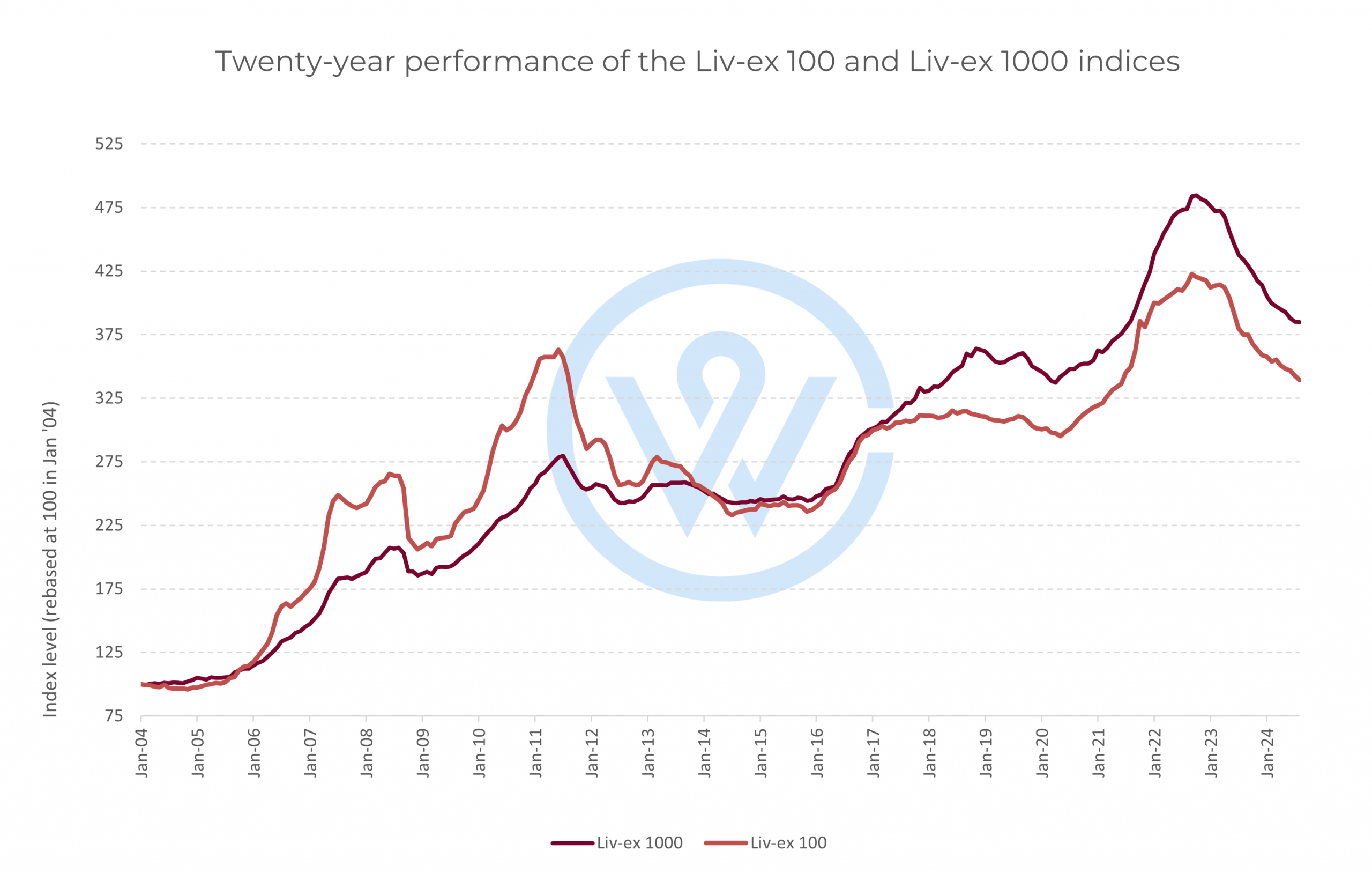

- After a three-year correction, fine wine prices are on the rise, signaling a prime entry point.

Over the past two decades, fine wine performance has been far from uniform, with returns driven by a distinct mix of liquidity, scarcity, and shifting global demand. The wines that have delivered the best ROI have done so for very different reasons, making a market breakdown essential to understanding where true value lies, and how each region behaves as an investment.

Bordeaux: The “S&P 500” of fine wine

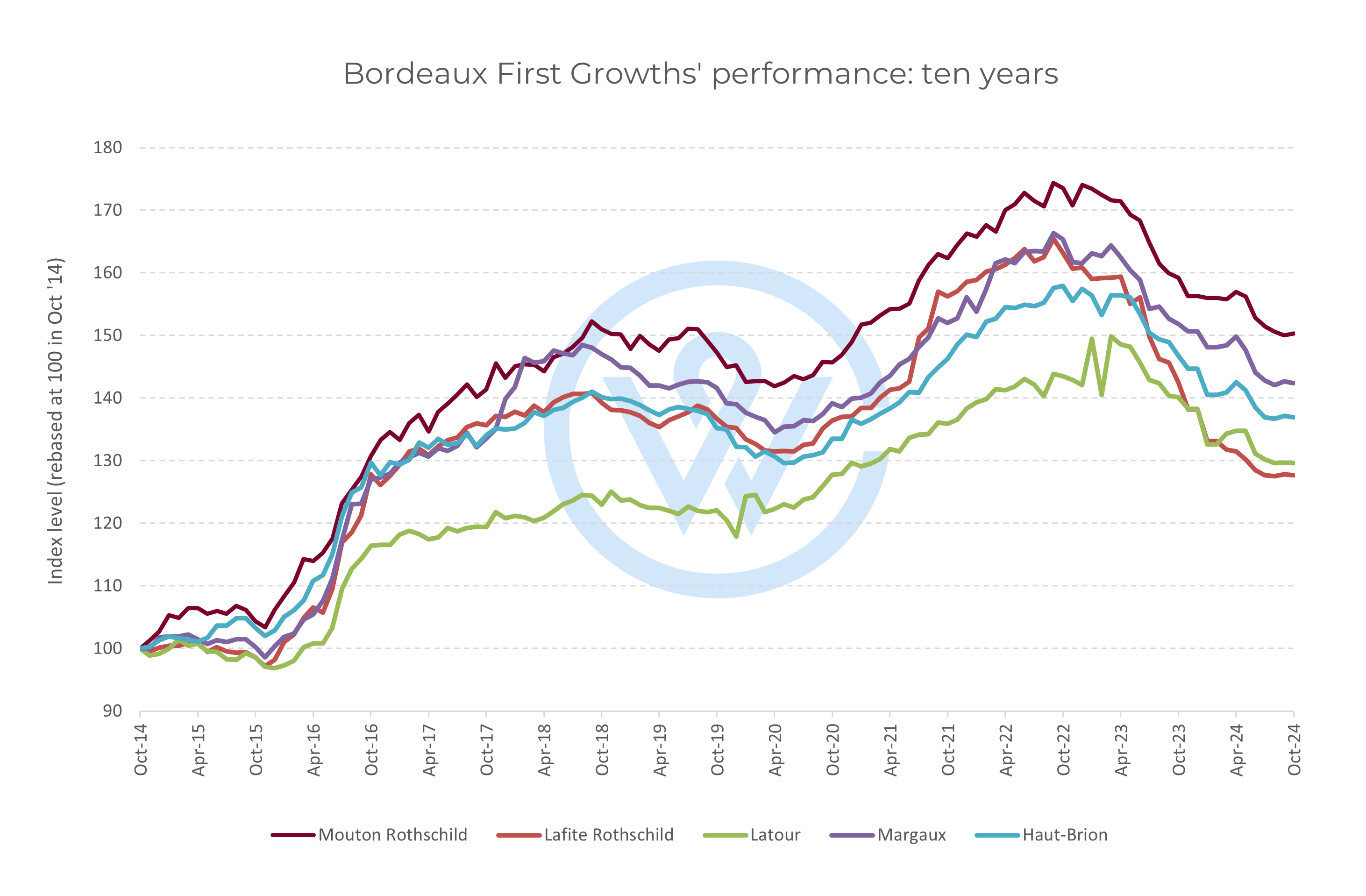

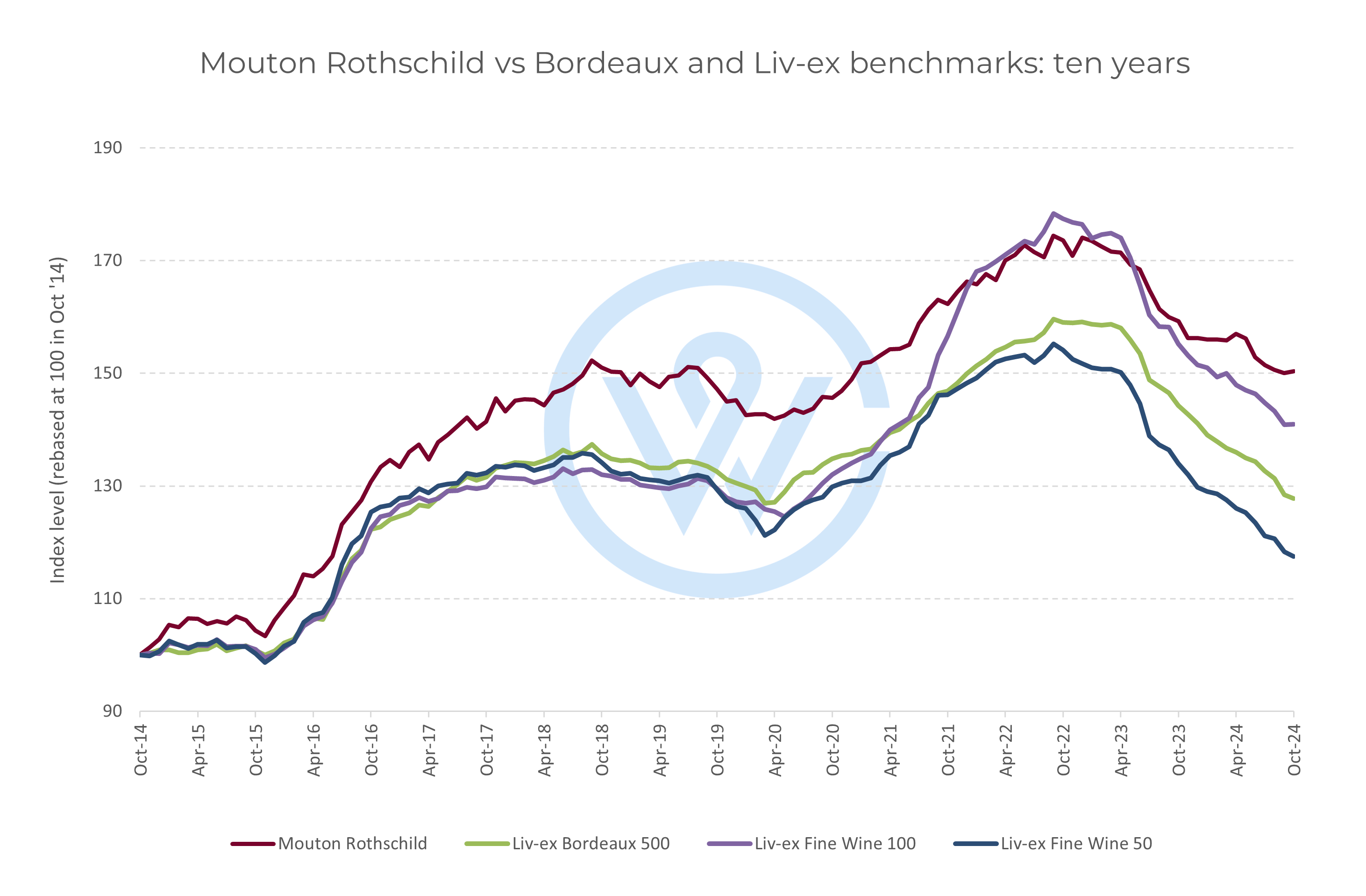

Bordeaux remains the cornerstone of the secondary wine market due to its high production volumes and global recognition. It provides a level of liquidity that acts as a defensive anchor, weathering the 2022-2025 correction better than most speculative assets.

- Le Pin

Located in Pomerol, this tiny estate is the absolute leader for the region. Growth from the 2013 bottom to the 2023 peak was over 130%, maintaining its value even during the recent “gut punch” of 2025.

- Carruades de Lafite

The second wine of Chateau Lafite Rothschild is a high-volume engine. The 2013 vintage, for instance, traded at £950 per case in 2014 and hit over £3,000 in 2022, marking a 215% return.

- Calon Segur

A historic Saint Estephe “hidden gem,” prices rose 120% in the ten years up to the 2023 peak and were more stable than many higher profile peers during the correction from 2023-2025.

Burgundy: Behind the stellar growth

The best historical performance can be found in Burgundy, where rarity meets intense global demand. However, investors must be wary of ghost wines that show huge growth on paper but offer very little real world liquidity.

- Domaine d’Auvenay

A personal estate of Lalou Bize-Leroy, also the owner of Domaine Leroy and part owner of Domane Romanee Conti, D’Auvenay produces wines of extraordinary intensity and rarity. “Aligote Sous Chatelet” is regarded as the best money can buy. At £30,000 a case, it is a significant asset. While liquidity is limited by small production levels, the price is backed by trades and auctions. It has shown a stunning 11,000% growth over its history. Auction prices for the 2009 vintage rose from £6,000 a case in 2019 to £35,000 in 2023.

- Domaine Bizot and Arnoux-Lachaux Jean-Yves Bizot

Both domaines produce tiny quantities of wine in Vosne-Romanee using natural winemaking techniques. They saw values soar in the late 2010s and early 2020s. For instance, Bizot Echezeaux 2010 rose from £4,000 in 2016 to £115,000 in 2022; however, few of these extreme values are backed by trades in the open market.

- Domaine de la Romanee-Conti (DRC)

Commonly known as DRC, Domaine de la Romanee-Conti is the most famous estate in Burgundy and the region’s benchmark for tradable and secure investment. Duvault Blochet is among their most affordable wines and their best performer. While 500% growth in ten years is modest compared to Bizot, DRC remains the most liquid and secure option for Burgundy investors.

The Champagne market: Grandes Marques and grower producers

The Champagne market shows a clear split between the Grandes Marques and grower producers. Large houses offer higher liquidity while grower Champagnes see lower trade volumes but often achieve bigger returns.

- Louis Roederer Cristal

Cristal is the flagship wine of the family owned house Louis Roederer. It was the best performer among the large producers in the decade leading to the 2022 market peak. Prices for Cristal increased 160% between 2016 and 2022.

- Krug Clos du Mesnil

This rare Blanc de Blancs is an example of the single vineyard wines that have become more common in the region over recent years. Clos du Mesnil leads the way in both prominence and performance, with prices up 215% from 2016 to the market top in 2022.

- Egly-Ouriet

The leader of the artisanal grower surge. Based in Ambonnay, this estate has seen values climb 500% over the last decade as collectors pivot toward terroir-driven grower Champagne.

Tuscany: Super Tuscans and Brunello

Tuscany provides a balance of high quality and relative value compared to French regions. The “Super Tuscan” category remains the primary driver of investment both among Italian wines, and within Tuscany.

- Sassicaia and Tignanello

Tignanello is produced by the historic Antinori family, while Sassicaia is the original Super Tuscan from Tenuta San Guido: these two labels lead the way for Italian wine liquidity. Both have proven to be excellent long-term investments and both have shown steady gains over 10 and 15 year periods. Tignanello has the slight edge, up 160% in the last decade.

- Il Marroneto Madonna delle Grazie

This Brunello di Montalcino is a more niche selection compared to the coastal Super Tuscans. Older vintages of this wine have risen upwards of 500% over the last decade.

- Soldera Casse Basse

The late Gianfranco Soldera created a cult following for his uncompromising approach to Sangiovese. This is one of the most expensive wines in Tuscany and has benefited from excellent growth, around 300% over the last decade. It remains just below the price of the 100% Merlot icon Masseto.

Piedmont: The “Burgundy of Italy”

Piedmont offers high growth but generally lower liquidity than Tuscany, mirroring the relationship between single-vineyard single-grape variety focus of Burgundy and the larger production volumes in Bordeaux.

- Comm G.B. Burlotto

The Burlotto family has made wine in Verduno for generations, but their Monvigliero has become a superstar. The wines of Burlotto are a highlight for the region. They have shown growth in the high hundreds of percentage points.

- Cappellano and Giovanni Canonica

These producers represent a traditional approach to Barolo that has found favour with modern collectors. Both have shown approximately 500% growth over the last decade. These names reflect the rising interest in terroir-driven, traditional Piedmont wine.

- Gaja

Angelo Gaja is the man credited with bringing Piedmont to the world stage through modernisation and high production levels compared to its regional peers. For investors and collectors, Gaja Barbaresco is a favourite. The wine has risen 100% in ten years, remaining solid since the 2022 market peak. Meanwhile, Gaja’s flagship white, Gaia and Rey, has seen nearly 400% growth over the last two decades.

USA: Cult wines and beyond

Cult wines often dominate the conversation in the United States. However, more mainstream brands have achieved equally impressive returns recently.

- Ridge Monte Bello

Ridge Vineyards is famous for its non-interventionist winemaking and focus on high altitude sites. They have a large selection of accessible wines, but Monte Bello is their flagship investment-grade label. Prices for Monte Bello are up 140% over the last 15 years.

- Opus One

Opus One was founded as a joint venture between Robert Mondavi and Baron Philippe de Rothschild. The estate focuses on producing large volumes of a single Grand Vin. This narrow focus has seen values double over the last decade.

- Screaming Eagle and Realm “The Absurd”

Screaming Eagle is the quintessential Napa Valley cult wine, produced in extremely small quantities. Lesser vintages, in particular, have proven to be strong performers: the 1998 saw 300% growth in the decade to 2021, while the 2011 vintage rose 240% between 2014 and 2021.

Realm Cellars produces “The Absurd” as a blend of their best barrels. It saw prices rise 300% in the decade to 2022.

High performers from other regions

Excellent growth is available outside the most mainstream regions. While liquidity tends to be more limited, these wines are standouts in their respective countries.

- Valentini Trebbiano d’Abruzzo

Valentini is a reclusive producer in Abruzzo known for creating whites with immense ageing potential. This white is the most searched for Italian fine wine outside of Piedmont and Tuscany and its index has risen 320% in the last decade.

- Chateau des Tours

This estate is under the same ownership as Chateau Rayas in Chateauneuf du Pape, but its wines are available at a much lower price. Their flagship, Vacqueyras, is roughly 10% of the price of Rayas, and while it does not achieve the same scores, values have risen 600% in a decade.

- Vega Sicilia Valbuena 5°

Vega Sicilia in the Ribera del Duero is perhaps the most prestigious estate in Spain and the best known to investors. Valbuena 5° is the younger sibling to the famous Unico, but its performance has consistently bettered its more costly sibling. It is up 47% over five years, 146% over ten years, and 215% over fifteen years.

- Sadie Family Columella

Eben Sadie is the leading figure in the new wave of South African winemaking. Their flagship, Columella, is up 140% in a decade. This eclipses other famous South African names like Klein Constantia Vin de Constance, up 60% in the same period.

- South America: Almaviva and Don Melchor

Almaviva is a joint venture between Baron Philippe de Rothschild and Concha y Toro in Chile. Both Almaviva and Don Melchor lead the way in South American investment performance. They have shown growth of around 200% in the last 15 years and 100% in the last decade.

FAQs: Which wines have the best ROI?

Which wine brand has the highest historical growth?

The highest percentage growth recorded in our analysis is Domaine d’Auvenay Aligote Sous Chatelet, which has seen stunning 11,000% gains over the last 20 years.

Is it better to invest in Bordeaux or Burgundy?

Bordeaux generally offers better liquidity and larger production volumes, making it easier to buy and sell. Burgundy has shown higher growth but can be more difficult to trade due to limited supply.

What is a ghost wine in the context of investment?

A ghost wine refers to a label that shows high price appreciation on paper but has very little actual trading volume or physical liquidity in the open market.

How has the US cult wine market performed recently?

While cult wines like Screaming Eagle have seen significant historical gains, more mainstream brands like Opus One have proven to be more reliable performers in recent years.

Are there profitable wine investments outside of France and Italy?

Yes, regions like Spain (Vega Sicilia), South Africa (Sadie Family), and Chile (Almaviva) have all produced wines with triple digit percentage growth over the last decade.

WineCap’s independent market analysis showcases the value of portfolio diversification and the stability offered by investing in wine. Speak to one of our wine investment experts and start building your portfolio. Schedule your free consultation today.